The Catalyst

The quantum complex went into this week carrying the single largest policy catalyst in its short public history. On June 22nd President Trump signed executive orders directing a whole-of-government push into quantum – one on hardware and sensing, one on cryptography.

The hardware directive stands up the Quantum Computer for Application Development and Discovery Science (QC-ADDS) programme, coordinating the Department of Energy with commerce, defence and intelligence agencies to deliver a science-relevant quantum computer to a national laboratory by 2028, with next-generation quantum sensors mandated by late 2028.

The cryptographic order is arguably the more consequential of the pair: it instructs federal agencies to begin migrating high-value systems to post-quantum cryptography, with deadlines into the 2030–2031 window and a Commerce pilot due by the end of 2027.

What changed on the 22nd was not the money – the $2 billion of allocated quantum funding had already been trailed in May – but the structure. A vague spending narrative became a calendar with named agencies and hard dates.

The U.S. government received equity stakes in exchange for the federal grants, this backing is not minor. It complies with the narrative of future growth and helps defend against the single biggest risk in the quantum industry: whether these companies can develop commercially viable machines before running out of cash.

Finanicals

The fundamentals have, to their credit, started to move. IonQ reported first-quarter revenue up roughly 755% year on year to $64.67m, which chief executive Niccolo de Masi called the biggest quarter in the company’s history. D-Wave posted quarterly bookings of $33.4m, a near twenty-fold increase driven by Fortune 100 and academic contracts. These are not pipeline promises; they are recognised revenue, formal bookings and signed federal paper.

Crucially, the balance sheets are funded. IonQ sits on roughly $3.5bn of cash, D-Wave on $588m and Rigetti on $569m with no debt. Unlike the large businesses involved in this sector, such as IBM, Google or Microsoft, none of these businesses generates the cash to self-fund – IonQ alone carried an EBITDA loss near $97m in the quarter – so that cash is raised, not earned, and shareholders wear the dilution. But it does remove the immediate solvency question and buys the sector years of runway to chase the milestones the executive orders have now dated.

Valuation

This is where the trade gets uncomfortable. Pure play, small capital companies like IonQ, D-wave and Regetti command market capitalisations of massive revenue multiples. On a price-to-sales basis the group has recently traded at multiples of roughly 100-800 times. This kind of pricing – paying an immense premium – is only sustained by the future earning potential of these companies.

Quantum computing proves beneficial for specific tasks, and is not as generally applicable as conventional silicon based computing. These tasks can generally fall into three groups.

- Quantum Simulation: Classical computers struggle to simulate the behaviour of molecules because of exponential mathematical complexity. Quantum computers natively replicate molecular interactions to accelerate drug discovery and design advanced materials like efficient solar cells or longer-lasting batteries.

- Complex Optimization: From global supply chain logistics to financial portfolio optimization, quantum computers can rapidly scan vast sets of variables and constraints to find the most mathematically optimal solutions.

- Cryptography & Security: While they can enhance data transmission security, sufficiently powerful quantum computers threaten current public-key encryption methods (like RSA). This capability is driving an industry-wide transition to post-quantum cryptography.

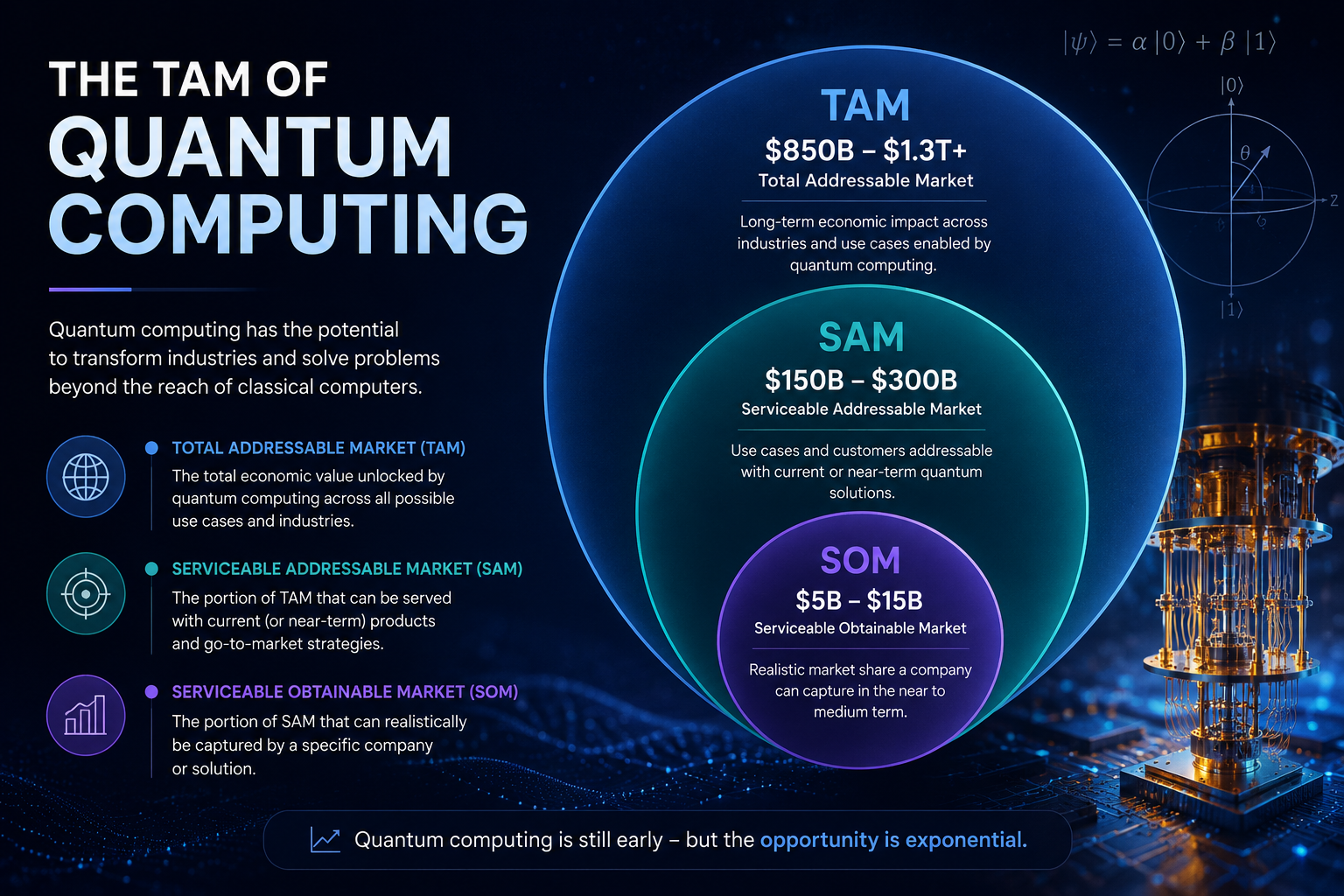

The total addressable market is set to expand, with estimations of how much varying dramatically. Current research and development within these companies is progressing and we now see some very specific tasks being better approached quantum mechanically.

The question ultimately comes down to how useful quantum computing will really be? Which architectural approach will provide the best foundation for future development? And how soon this computation becomes commercially viable?

Industry

The market currently treats IonQ, Rigetti, D-Wave and Quantum Computing Inc. as a single basket, despite each running a fundamentally different architecture – trapped ions, superconducting gates, quantum annealing and photonics respectively. That correlation is a sentiment artefact, not a fundamental one, and it is where the real risk and opportunity sit.

The unresolved question for the decade is whether commercial quantum is captured by these pure-plays or by the mega-caps quietly out-resourcing them: IBM’s 156-qubit Heron R2 targeting a quantum-advantage demonstration this year and fault-tolerance by 2029, Google’s Willow chip clearing the error-correction threshold, and Microsoft’s topological Majorana bet. Nvidia’s CUDA-Q platform, which folds quantum error correction into existing GPU data-centre workflows, is the connective tissue that could make any winner’s output usable – and a reminder that the incumbents do not need quantum to work next year to keep compounding.

The comparison to the dot-com build-out cuts differently here than it did for Micron’s recent Q3 earnings. With memory, current earnings justify the valuation. With quantum, investors are buying an option on a technology that most researchers still place a decade from broad commercial usefulness. The science is advancing in genuine steps; the business case is not yet at scale.

Market Signals These are among the highest-beta names on the tape – a function of concentrated floats, heavy retail ownership and options dealers hedging into thin liquidity. The June 23rd pop has already given background, which is characteristic: the basket sprints on headlines and consolidates on delivery.

Two near-term risks are worth flagging into the week. First, the financial first half closes on June 30th, and the quantum cohort has been one of the strongest momentum trades of the quarter – exactly the kind of position large institutions lock in and rebalance, which can manufacture selling pressure independent of the story. Second, with the catalyst now priced, the next leg needs delivery: independent benchmarks, renewing multi-year contracts and margin progression, not another headline.

The executive orders are a real de-risking of the long-term thesis. They are not a valuation. The fundamentals are accelerating and the runway is funded, but the multiples already discount a future that is years and several technical milestones away.