Financials

Micron released their Q3 2026 earnings on June 24th, with the quarter ending May 28th. The quarter was remarkable and reaffirmed the massive demand in the memory industry.

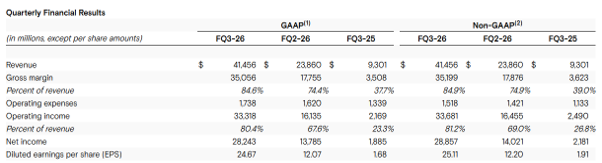

Micron’s revenue rose to 41.5 billion USD gaining 350% year on year over the same period. Similarly non-GAAP net income rose 1200% to 25.11 USD per diluted share with an 84.9% gross margin - more in line with the historically high margins of the software industry. Other financial metrics beat expectations across the board, with subsequent Q4 guidance sitting even stronger. The overhanging question of peak earnings has resoundingly been answered on Wednesday’s print. In terms of business by technology, DRAM made up 76% of total revenue - 31.3 billion USD and NAND 24% - 9.9 billion USD, these two technologies’ revenue increased 67% and 99% quarter on quarter. MU expects to see 10 billion USD of capital expenditure in Q4 to expand supply to meet the historic memory demand. The business is massively cash positive now with 6.38 billion USD in debt, 18.84 billion USD in cash and equivalents and free cash flow of 17.56 billion USD. Micron forecasts this cash flow to increase substantially further into Q4 and expects to return 100% of excess cash to shareholders over time. It is clear Micron has proved very fruitful over recent time but how should this newly trillion-dollar company be valued? And how should the industry as a whole respond to this signal?

Cyclicality

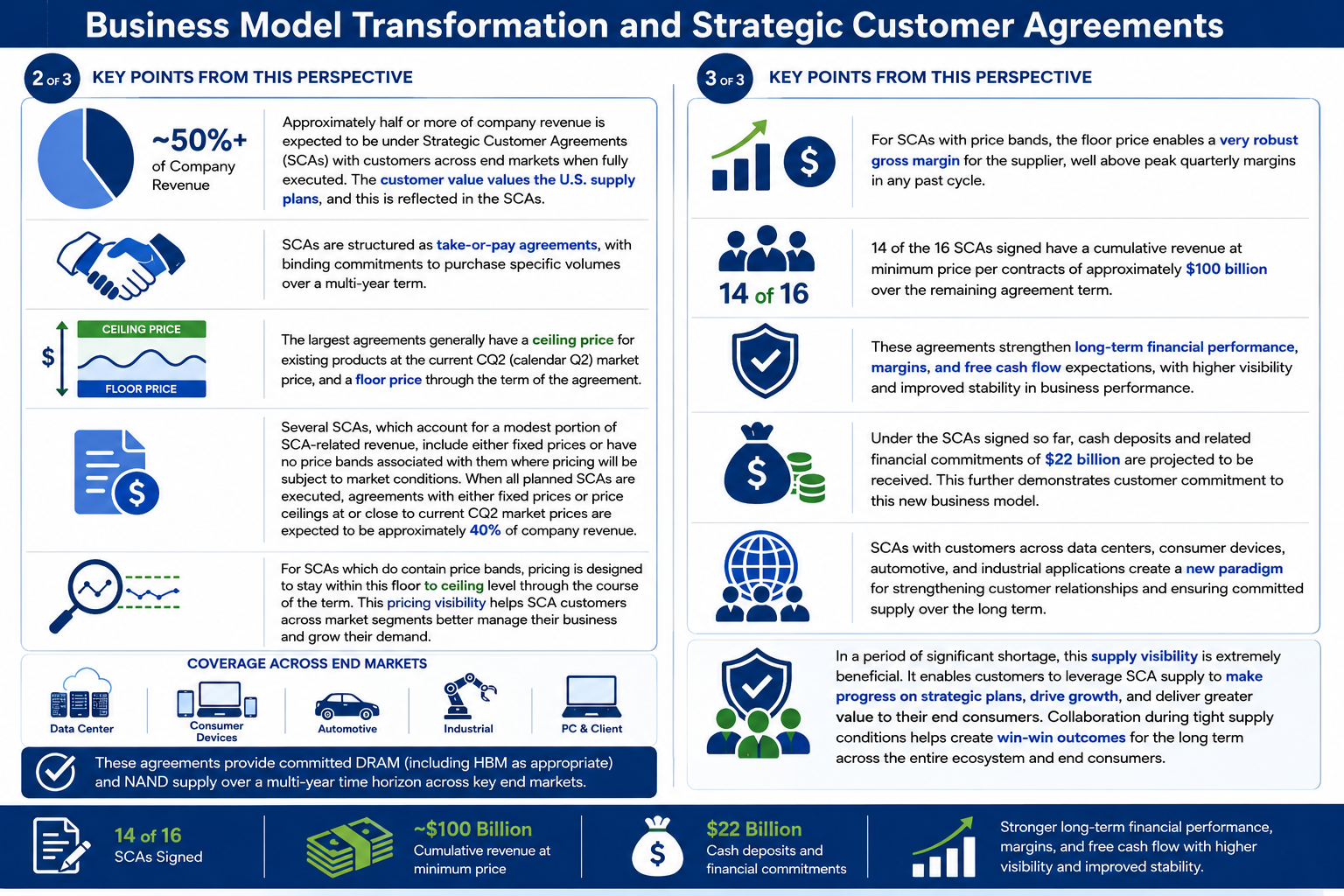

The memory industry has been historically cyclical with demand driving buildout then supply chasing the demand until the supply is heavy. For this reason, the memory industry has traded at a low P/E ratio in comparison to indices such as the S&P 500. Recently this P/E ratio has increased to agree with those of other large market cap companies due to the immense growth observed within the sector. This P/E ratio still lies below that of the market average across the S&P 500, but the speculation of cyclicality remains. It seems probable the cyclical nature will remain but it is a matter of how long such a cycle lasts that can dictate how the company could be valued in a shorter timeframe. Micron does not see significant supply expansion completion until early 2028 and so assuming AI buildout continues – MU can reap the benefits for at minimum a year to come. Micron has pioneered the development of SCAs or strategic customer agreements, which enhance partnerships and supply customers with a contracted supply assurance over some time – typically a 5-year period or 3 to the automotive industry. 16 of such agreements are signed at the current time and make up 20% of the DRAM volume or one third of the NAND volume. These SCAs have the potential to significantly change the nature of the memory trade and ensure revenue for time to come, potentially warranting a less discounted P/E to which the industry historically suffers.

Industry

The semiconductor boom we are witnessing into the AI buildout is historic and closely compared to the ‘dot com bubble’. Unlike the ‘dot com bubble’, however, company earnings speak for the valuation and the valuation of the companies benefitting is generally backed by improved business. Of course, the question as to whether the AI end-product will drive the revenue hoped for to warrant such capital expenditure remains, but there is no sign of slowing capital expenditure from hyper-scalers such as AMZN, GOOG and MSFT. And so there is, as of yet, no signalling of stalling buying pressure towards these semiconductor companies. In fact, the expected expenditure YoY is increasing dramatically 2025-2026. MU’s earnings is not a sign to be looked upon negatively when considering their competition but is a sign that the story remains intact and likely hints that we will see strong earnings across peers such as SK Hynix, Samsung, SNDK and more.

Market Signals

Micron and the surrounding market often trade down on earnings; however, June 24th was different into open on the 25th. The stock and sector gained sharply before giving much of the gain back on Friday’s close (26th). The long-term valuation provided by such earnings warrants a higher valuation than that of the current trading price of MU, but the short-term semiconductor market is choppy and has risen sharply. With the financial Q2 of 2026 wrapping up the 30th of June, large institutions could lock in profits and rebalance which could drive some heavy selling pressure as seen on the 26th. On the 26th the SOXX closed below the 22 SMA preceded by a gap down from the 25th. This sets up a bearish dynamic into the weekend despite the strong earnings signalling from MU.